Free 3015 1 Minnesota Template

Free 3015 1 Minnesota Template

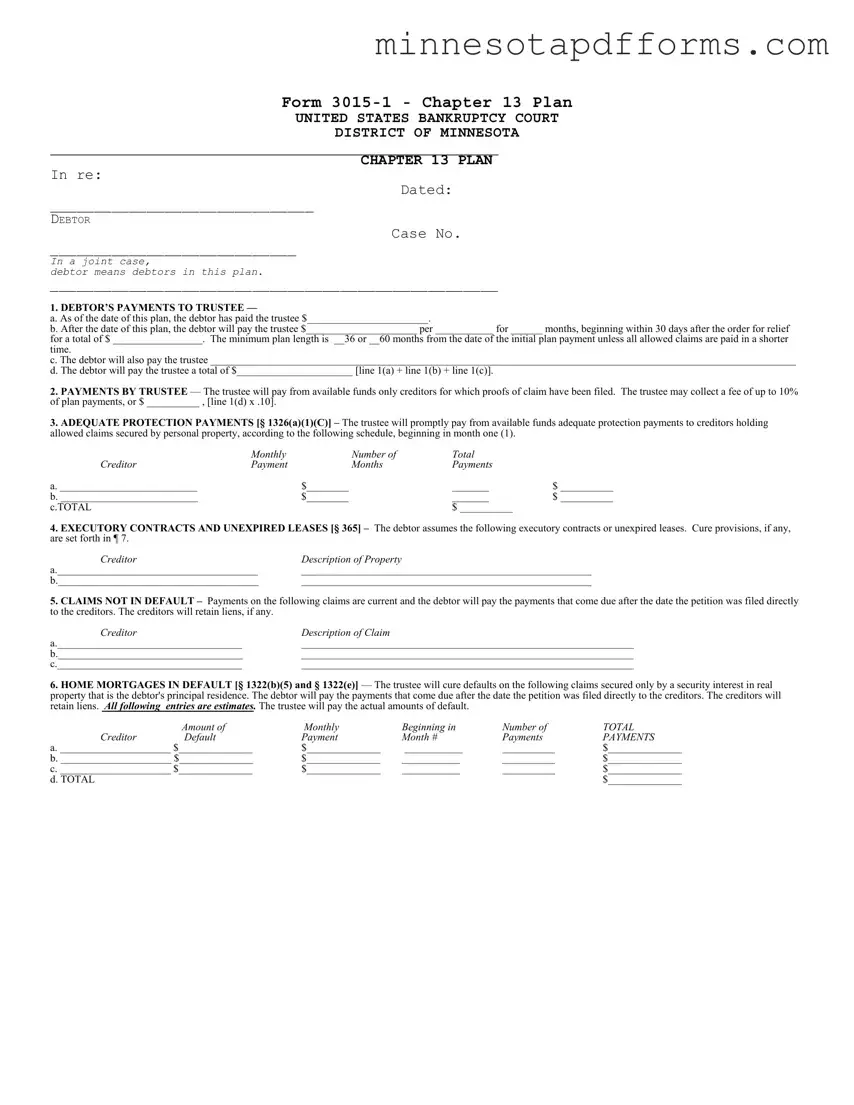

The Form 3015-1 in Minnesota, known as the Chapter 13 Plan, serves as a detailed blueprint for managing a debtor's financial obligations under Chapter 13 bankruptcy in the United States Bankruptcy Court for the District of Minnesota. This form outlines an intricate plan for debt repayment, including initial payments made to the trustee, ongoing monthly payments, and additional conditions based on the debtor's unique financial scenario. It details the debtor's commitment to the trustee regarding payment amounts and schedules, starting within 30 days after the order for relief and spanning a minimum length of either 36 or 60 months, unless all allowed claims can be resolved sooner. Payments the trustee will make on the debtor’s behalf, the treatment of secured claims, executory contracts, unexpired leases, claims in default, and the provision for priority and unsecured claims are all systematically laid out. The form further addresses the procedure for claims deemed in default, the hierarchy of creditor repayments, and various protections for creditors, ensuring that the allowed secured claims maintain their priority and that adequate protection payments are made promptly. Additionally, the form delineates the responsibilities for curing defaults on secured debts, particularly those secured by the debtor's principal residence, and establishes the treatment of tardily filed unsecured creditors, with any residual funds managed at the trustee’s discretion. This document encapsulates a comprehensive plan for reorganizing and repaying debtor obligations, intending to facilitate a structured path towards financial recovery under the oversight of the court.

Form

UNITED STATES BANKRUPTCY COURT

DISTRICT OF MINNESOTA

CHAPTER 13 PLAN

IN RE:

DATED:

______________________________

DEBTOR

CASE NO.

____________________________

In a joint case,

debtor means debtors in this plan.

___________________________________________________

1. DEBTOR’S PAYMENTS TO TRUSTEE —

a. As of the date of this plan, the debtor has paid the trustee $_______________________.

b. After the date of this plan, the debtor will pay the trustee $_____________________ per ___________ for ______ months, beginning within 30 days after the order for relief

for a total of $ _________________. The minimum plan length is __36 or __60 months from the date of the initial plan payment unless all allowed claims are paid in a shorter

time.

c. The debtor will also pay the trustee _______________________________________________________________________________________________________________

d. The debtor will pay the trustee a total of $______________________ [line 1(a) + line 1(b) + line 1(c)].

2.PAYMENTS BY TRUSTEE — The trustee will pay from available funds only creditors for which proofs of claim have been filed. The trustee may collect a fee of up to 10% of plan payments, or $ __________ , [line 1(d) x .10].

3.ADEQUATE PROTECTION PAYMENTS [§ 1326(a)(1)(C)] – The trustee will promptly pay from available funds adequate protection payments to creditors holding allowed claims secured by personal property, according to the following schedule, beginning in month one (1).

|

Monthly |

Number of |

Total |

|

Creditor |

Payment |

Months |

Payments |

|

a. __________________________ |

|

$________ |

_______ |

$ __________ |

b. __________________________ |

|

$________ |

_______ |

$ __________ |

c.TOTAL |

|

|

$ __________ |

|

4.EXECUTORY CONTRACTS AND UNEXPIRED LEASES [§ 365] – The debtor assumes the following executory contracts or unexpired leases. Cure provisions, if any, are set forth in ¶ 7.

Creditor |

Description of Property |

a.______________________________________ |

_______________________________________________________ |

b.______________________________________ |

_______________________________________________________ |

5.CLAIMS NOT IN DEFAULT – Payments on the following claims are current and the debtor will pay the payments that come due after the date the petition was filed directly to the creditors. The creditors will retain liens, if any.

Creditor |

Description of Claim |

a.___________________________________ |

_______________________________________________________________ |

b.___________________________________ |

_______________________________________________________________ |

c.___________________________________ |

_______________________________________________________________ |

6.HOME MORTGAGES IN DEFAULT [§ 1322(b)(5) and § 1322(e)] — The trustee will cure defaults on the following claims secured only by a security interest in real property that is the debtor's principal residence. The debtor will pay the payments that come due after the date the petition was filed directly to the creditors. The creditors will retain liens. All following entries are estimates. The trustee will pay the actual amounts of default.

|

Amount of |

Monthly |

Beginning in |

Number of |

TOTAL |

Creditor |

Default |

Payment |

Month # |

Payments |

PAYMENTS |

a. _____________________ $______________ |

$______________ |

___________ |

__________ |

$______________ |

|

b. _____________________ $______________ |

$______________ |

___________ |

__________ |

$______________ |

|

c. _____________________ $______________ |

$______________ |

___________ |

__________ |

$______________ |

|

d. TOTAL |

|

|

|

|

$______________ |

7.CLAIMS IN DEFAULT [§ 1322 (b)(3) and (5) and § 1322(e)] — The trustee will cure defaults on the following claims as set forth below. The debtor will pay the payments that come due after the date the petition was filed directly to the creditors. The creditors will retain liens, if any. All following entries are estimates, except for interest rate.

|

Amount of |

|

Int. rate |

Monthly |

Beginning in |

Number of |

|

TOTAL |

|

|

Creditor |

Default |

(if applicable) |

Payment |

Month # |

|

Payments |

|

PAYMENTS |

||

a. _____________________ $______________ |

____ |

$______________ |

__________ |

|

__________ |

$_______________ |

||||

b. _____________________ $______________ |

____ |

$______________ |

__________ |

__________ |

$_______________ |

|||||

c. _____________________ $______________ |

____ |

$______________ |

__________ |

__________ |

$_______________ |

|||||

d. TOTAL |

|

|

|

|

|

|

|

|

$_______________ |

|

8.OTHER SECURED CLAIMS; SECURED CLAIM AMOUNT IN PLAN CONTROLS [§ 1325(a)(5)] — The trustee will pay, on account of the following allowed secured claims, the amount set forth in the “Total Payments” column, below. The creditors will retain liens securing the allowed secured claims until the earlier of the payment of the underlying debt determined under nonbankruptcy law, or the date of the debtor’s discharge. NOTWITHSTANDING A CREDITOR'S PROOF OF CLAIM FILED BEFORE OR AFTER CONFIRMATION, THE AMOUNT LISTED IN THIS PARAGRAPH AS A CREDITOR'S SECURED CLAIM BINDS THE CREDITOR PURSUANT TO 11 U.S.C. § 1327, AND CONFIRMATION OF THE PLAN IS A DETERMINATION OF THE CREDITOR'S ALLOWED SECURED CLAIM.

|

|

|

|

Beginning |

( Number |

|

Payments |

|

(Adequate |

|

|

|

Claim |

Secured |

Int. |

in |

( Monthly |

X of |

= |

on Account |

|

+ Protection |

= TOTAL |

Creditor |

Amount |

Claim |

|

Rate |

Month # |

Payment) |

Payments) |

of Claim |

from ¶ 3) |

||

PAYMENTS |

|

|

|

|

|

|

|

|

|

|

|

a. __________________ $_____________ $_______________ |

___ |

______ |

$______ |

__________ |

$__________ |

$________ |

$________ |

||||

b. __________________ $_____________ $_______________ |

___ |

______ |

$______ |

__________ |

$__________ |

$________ |

$________ |

||||

c. __________________ $_____________ $_______________ |

___ |

______ |

$______ |

__________ |

$__________ |

$________ |

$________ |

||||

d. TOTAL |

|

|

|

|

|

|

|

|

|

|

$________ |

9.PRIORITY CLAIMS — The trustee will pay in full all claims entitled to priority under § 507, including the following. The amounts listed are estimates. The trustee will pay the amounts actually allowed.

|

Estimated |

Monthly |

Beginning in |

Number of |

TOTAL |

|

Creditor |

Claim |

Payment |

Month # |

Payments |

|

PAYMENTS |

a. Attorney Fees |

$______________ |

$______________ |

___________ |

__________ |

$______________ |

|

b. Domestic support |

$______________ |

$______________ |

___________ |

__________ |

$______________ |

|

c. IRS |

$______________ |

$______________ |

___________ |

__________ |

$______________ |

|

d. MN Dept. of Rev. |

$______________ |

$______________ |

___________ |

__________ |

$______________ |

|

e. _________________ $______________ |

$______________ |

___________ |

__________ |

$_____________ |

||

f. TOTAL |

|

|

|

|

|

$______________ |

10.SEPARATE CLASSES OF UNSECURED CREDITORS — In addition to the class of unsecured creditors specified in ¶ 11, there shall be separate classes of

The trustee will pay the allowed claims of the following creditors. All entries below are estimates.

|

Interest |

|

|

|

|

|

|

Rate |

Claim |

Monthly |

Beginning in |

Number of |

TOTAL |

Creditor |

(if any) |

Amount |

Payment |

Month # |

Payments |

PAYMENTS |

a.______________ |

____ |

_______ |

________ |

________ |

_______ |

$ _____________ |

b.______________ |

____ |

_______ |

________ |

________ |

_______ |

$ _____________ |

c. TOTAL |

|

|

|

|

|

$ _____________ |

11.TIMELY FILED UNSECURED CREDITORS — The trustee will pay holders of nonpriority unsecured claims for which proofs of claim were timely filed the balance of all payments received by the trustee and not paid under ¶ 2, 3, 6, 7, 8, 9 and 10 their pro rata share of

approximately $______________ [line 1(d) minus lines 2, 6(d), 7(d), 8(d), 9(f), and 10(c)].

a. The debtor estimates that the total unsecured claims held by creditors listed in ¶ 8 are $_____________________.

b. The debtor estimates that the debtor's total unsecured claims (excluding those in ¶ 8 and ¶ 10) are $__________________. c. Total estimated unsecured claims are $______________ [line 11(a) + line 11(b)].

12.

13.OTHER PROVISIONS — The trustee may distribute additional sums not expressly provided for herein at the trustee’s discretion.

14.SUMMARY OF PAYMENTS —

Trustee's Fee [Line 2) |

. . . . . . . . . . . . …. . . . . . . . . . . . . $ ________________________________ |

Home Mortgage Defaults [Line 6(d)] |

. . . . . . . . . . . . . . . . . . . . . . . . . ... $ ________________________________ |

Claims in Default [Line 7(d)] |

……….. . . . . . . . . . . . . . . . ... . . $ ________________________________ |

Other Secured Claims [Line 8(d)] |

………………………….... . . . . . $ ________________________________ |

Priority Claims [Line 9(f)] |

. . . . . . . . . . . . . . . ……. . . . . . . $ ________________________________ |

Separate Classes [Line 10(c)] |

. . . . . . . . . . . . . . . . . . . . . . . . . . . $ ________________________________ |

Unsecured Creditors [Line 11] |

. . . . . . . . . . . . . . . . . . . . ….. . . . . $ ________________________________ |

TOTAL [must equal Line 1(d)] |

. . . . . . . . . . . .. . . . . . . . . . . . . . . . $ ________________________________ |

Insert Name, Address, Telephone and License Number of Debtor's Attorney: |

|

|

Signed________________________________________________ |

|

DEBTOR |

|

Signed________________________________________________ |

|

DEBTOR (if joint case) |

| Fact | Detail |

|---|---|

| Document Title | Chapter 13 Plan Form 3015-1 |

| Court | United States Bankruptcy Court District of Minnesota |

| Purpose | Outlines the repayment plan for a debtor under Chapter 13 bankruptcy |

| Initial Payment Timing | Beginning within 30 days after the order for relief |

| Minimum Plan Length | 36 or 60 months from the date of the initial plan payment unless all allowed claims are paid sooner |

| Trustee's Fee Cap | Up to 10% of plan payments |

| Adequate Protection Payments | Payments made to creditors with allowed claims secured by personal property |

| Executory Contracts and Unexpired Leases | Assumptions and cure provisions for contracts and leases in the plan |

| Home Mortgages in Default | Plan to cure defaults on mortgage claims secured by the debtor's principal residence |

| Governing Law | Guided by Title 11 of the United States Code (Bankruptcy Code) |

Filling out form 3015-1, the Chapter 13 Plan form for the United States Bankruptcy Court District of Minnesota, is a crucial task that should be approached with care. This document outlines the payment plans and terms for individuals who are restructuring their debt under Chapter 13 bankruptcy proceedings. The information provided within serves as a blueprint for how the debtor intends to manage and pay back their obligations. Below are the steps needed to correctly fill out this form.

Once the form is fully completed, it should be reviewed for accuracy and completeness. The debtor and their attorney need to ensure that all payments and provisions are correctly calculated and clearly described to meet the court’s requirements and help facilitate the bankruptcy process.

What is Form 3015-1?

Form 3015-1, known as the Chapter 13 Plan, is a legal document filed in the United States Bankruptcy Court for the District of Minnesota. It is used by individuals (referred to as the debtor or debtors in joint cases) to propose a plan for repayment of their debts over a certain period, under Chapter 13 bankruptcy protection. This plan outlines how the debtor intends to make payments to the trustee, who then distributes these payments to creditors according to the plan’s specifications.

How does a debtor make payments to the trustee under this plan?

According to the plan, payments to the trustee are made in two parts: the amount already paid as of the date of the plan and future payments. The debtor agrees to pay a specified amount per month for a duration outlined in the plan, starting within 30 days after the order for relief. The total amount paid to the trustee is a sum of the initial payment made, future monthly payments, and any additional payments as outlined in the plan.

What types of debts are repaid through the Chapter 13 Plan?

Several types of debts are addressed in the Chapter 13 Plan, including:

What is the minimum plan length for a Chapter 13 Plan?

The minimum plan length for a Chapter 13 Plan according to Form 3015-1 can be either 36 or 60 months from the date of the initial payment. This timeframe is based on the debtor's financial situation and the type of debts being repaid. The actual length might vary if all allowed claims are paid in a shorter time period.

Can the trustee pay creditors not listed in the plan?

Yes, the trustee has the discretion to distribute additional sums to creditors not expressly named in the plan if there are funds available after fulfilling the outlined payments. This capability allows the trustee to address claims that may arise or become known after the plan is confirmed by the court.

What happens if a proof of claim is filed after the plan is confirmed?

Even if a creditor's proof of claim is filed before or after the plan is confirmed, the amounts listed in the plan for secured claims bind the creditor, pursuant to 11 U.S.C. § 1327. The confirmation of the plan thereby serves as a determination of the creditor's allowed secured claim, ensuring that the plan's provisions regarding debt repayment are adhered to.

Filling out the Minnesota Form 3015-1, a Chapter 13 Plan, is a crucial step in managing bankruptcy. However, it's easy to make errors that can affect the bankruptcy process. Here are eight common mistakes people make when completing this form:

To avoid these mistakes, it's recommended to review the form carefully, double-check calculations, and ensure all required information is complete and accurate. Consultation with a bankruptcy attorney can also help clarify any questions and ensure the form is filled out correctly.

When navigating the complexities of Chapter 13 bankruptcy in Minnesota, utilizing Form 3015-1 is just the starting point. A variety of other forms and documents often accompany this form to ensure comprehensive coverage of one's financial situation and legal obligations. Each document plays a crucial role in providing the court with detailed insights into the debtor's financial obligations, assets, and the proposed plan for reorganization and repayment of debts.

The 3015-1 Minnesota form, known as the Chapter 13 Plan, shares features with several other legal documents, each designed for specialized purposes within the realm of U.S. bankruptcy law. One notable document is the Chapter 7 Statement of Financial Affairs. This document also requires detailed financial information from the debtor, similar to how the Chapter 13 Plan necessitates a comprehensive outline of the debtor's payment strategy to the trustee. Both documents aim to give the court a clear picture of the debtor's financial situation, but while the Chapter 13 Plan focuses on repayment plans, the Chapter 7 document is more about assessing the eligibility for liquidation of assets.

The Proof of Claim form, another critical document in bankruptcy cases, bears resemblance to the 3015-1 form in that it allows creditors to officially declare the amount owed by the debtor. Where the Chapter 13 Plan outlines how debts, including those verified by a Proof of Claim, will be repaid, the Proof of Claim itself is the step that enables creditors to assert their rights to receive payments. This interconnection ensures that the repayment plan is comprehensive and accounts for all claims recognized by the bankruptcy court.

Similarly, the Chapter 13 Plan shares similarities with the Application for Payment of Unclaimed Funds. While the latter is used when creditors or other stakeholders are due payments from bankruptcy cases that have been unclaimed, the structure and intent behind both documents involve the distribution of funds in accordance with bankruptcy law procedures. Both aim to ensure creditors are paid in an orderly and fair manner, under the supervision of the court.

The Reaffirmation Agreement document is also akin to the Chapter 13 Plan. It's used when a debtor decides to continue paying a dischargeable debt, like a car loan, to retain the asset. Even though the nature of these documents differ—the Reaffirmation Agreement focuses on individual debts and the Chapter 13 Plan on the aggregated repayment effort—both involve renegotiated payment terms approved by the bankruptcy court, highlighting the debtor's intention to manage their debts responsibly.

Finally, the Modification of Chapter 13 Plan is a document that directly correlates with the original 3015-1 form, as it outlines changes to the debtor's repayment plan post-approval. Modifications may be necessary due to changes in the debtor's financial situation or to correct oversights in the initial plan. This highlights not just a structural similarity but a procedural one, emphasizing the dynamism of bankruptcy cases and the need for documents that can adapt to unfolding financial circumstances.

When filling out the Form 3015-1 Minnesota, navigating the intricacies can feel daunting. Here are some essential dos and don'ts to help ensure accuracy and completeness in the process:

By adhering to these guidelines and proceeding with diligence, you'll navigate the form's complexities more effectively, contributing to a smoother chapter 13 process.

When navigating bankruptcy filings, particularly the Chapter 13 Plan outlined in Form 3015-1, individuals often come across several misconceptions. Understanding these can provide clarity on the process and the plan’s requirements. Below are nine common misconceptions about the 3015-1 Minnesota form:

Understanding these misconceptions and the facts behind Form 3015-1 can simplify the bankruptcy process, making it more approachable for individuals seeking relief under Chapter 13. It’s advisable for debtors to familiarize themselves with the specifics of the form and seek professional advice if needed to ensure that all legal requirements are properly met.

Filling out and using Form 3015-1, the Chapter 13 Plan for the District of Minnesota, requires understanding its purpose and components. Here are six key takeaways to consider:

Form 3015-1 serves as a comprehensive roadmap for debtors and trustees in Chapter 13 bankruptcy cases, ensuring that the repayment plan is structured, transparent, and considers the rights and interests of all parties involved.

Minnesota Urolith Center - Stresses the importance of obtaining direct samples from both upper and lower urinary tracts when possible, for comprehensive analysis.

Mncred - This form is designed for the reappointment of physicians, dentists, and allied health professionals in Minnesota.

Minnesota Sales and Use Tax - Engage with Minnesota’s sales tax requirements accurately by providing full disclosure of your business activities on form ST101.