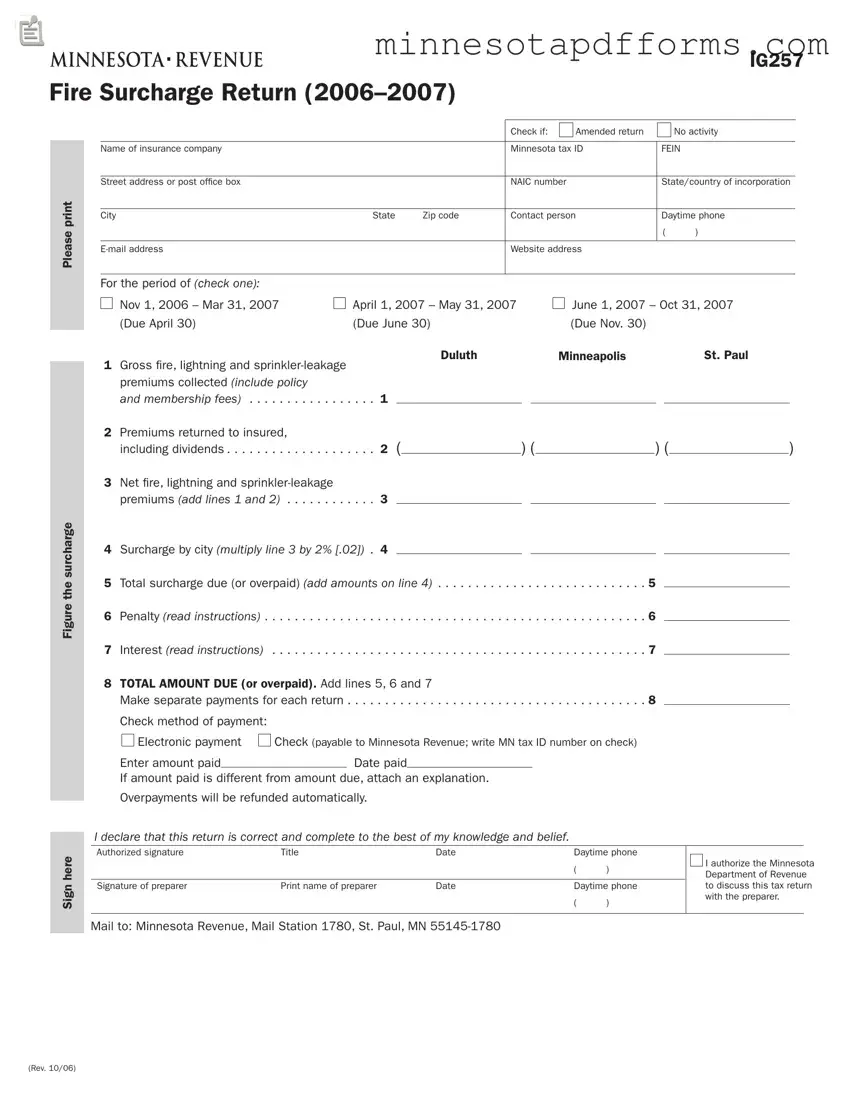

Filing requirements

The surcharge applies to insurance coverage written on risks located in Duluth, Min- neapolis and St. Paul. All insurers licensed to write ire, lightning and sprinkler leakage insurance in Minnesota must ile a return even if no ire business was done in the three cities during the period indicated.

The amount of the surcharge must be shown as a speciic item on the face (declaration page), daily report, endorse- ments and billing notice of each policy. The surcharge applies to all additional ire, lightning and sprinkler-leakage premi- ums unless exempt from the surcharge as explained below.

The surcharge is equal to 2 percent of all ire, lightning and sprinkler-leakage gross premiums, less return premiums on all di- rect business from property located within Duluth, Minneapolis or St. Paul city limits. The surcharge is not collected on premiums for auto or aircraft ire insurance, marine ire insurance, or other property in transit.

If a premium is returned to the insured, recalculate the surcharge on the same basis the original surcharge was calculated.

The surcharge is paid by the insured and must be forwarded to the Department of Revenue by the insurance company. The in- surance company cannot pay the surcharge for the insured. The surcharge is not subject to a commission charge by the agent or a tax by the state.

The following methods should be used to report the ire, lightning and sprinkler-leak- age premiums separately for policies carry- ing multiple peril premiums.

•Farm owners mutiple-peril policies. The surcharge is based on 35 percent of the premiums.

•Homeowners multiple-peril policies. The surcharge is based on 35 percent of the premiums.

•Commercial non-liability coverages. The surcharge is based on 55 percent of the premiums.

•Commercial liability policies. The surcharge is based on 35 percent of the premiums.

Due dates

The surcharge return for the period ending March 31 is due April 30. The return for the period ending May 31 is due June 30. The return for the period ending October 31

is due November 30. Please make sepa- rate electronic payments or write separate checks for each period.

The U.S. postmark date, or date recorded or marked by a designated delivery service, is considered the iling date (private postage meter marks are not valid). When the due date falls on a Saturday, Sunday, or legal holiday, returns postmarked on the next business day are considered on time. When a return is iled late, the date it is received at the Department of Revenue is treated as the date iled.

Electronic payments

You’re required to pay electronically this year if your total taxes and surcharges due for the last calendar year exceeded $120,000.

You must also pay electronically if you’re required to pay ANY Minnesota business tax electronically, such as sales or withholding tax.

To pay over the Internet, go to www.taxes. state.mn.us and click “Login to e-File Min- nesota” on the e-Services menu. If you don’t have Internet access, you can pay by phone at 1-800-570-3329. You’ll need your bank routing and account numbers.

To pay by other electronic payment methods, such as ACH credit method or Fed Wire, call our ofice for instructions. Please submit separate payments for each return.

Information and assistance

If you need additional information or help to complete this form, call 651-297-1772 or e-mail insurance.taxes@state.mn.us.

TTY: Call 711 for Minnesota Relay. We’ll provide information in other formats upon request to persons with disabilities.

Forms are available on our website at www. taxes.state.mn.us.

Instructions

Check boxes

At the top of the form, check if the return is:

•An Amended Return: Check only if you are amending a previously iled return for the same period.

•For No Activity: Check only if you did not collect premiums for any insurance that had ire, lightning or sprinkler-leak- age coverage.

Line instructions

Line 6

Penalties

Late payment. If you ile on time but don’t pay all the tax due by the due date, a late payment penalty is due. The penalty is

5 percent of the unpaid tax for any part of the irst 30 days the payment is late, and

5 percent for each additional 30-day period, up to a maximum of 15 percent.

Late filing. Add a late iling penalty to the late payment penalty if your return is not iled by the due date. The penalty is

5 percent of the unpaid tax. When added to the late payment penalty, the maximum combined penalty is 20 percent.

Payment method. If you are required to pay electronically and do not, an additional 5 percent penalty applies to payments not made electronically, even if a paper check is sent on time.

Line 7

Interest

You must pay interest on the unpaid tax plus penalty from the due date until the total is paid. The interest rate for calendar year 2007 is 8 percent. The interest rate may change for 2008. To igure how much inter- est you owe, use the following formula with the appropriate interest rate:

Interest =

(tax + penalty) x # of days late x interest rate ÷ 365