Free Minnesota Ig260 Template

Free Minnesota Ig260 Template

Navigating the complexities of the Minnesota IG260 form, a pivotal document for surplus lines brokers engaging in nonadmitted insurance transactions, demands a thorough understanding. Spanning the reporting periods of January 1 to June 30 and July 1 to December 31, this form serves as the 2021 Nonadmitted Insurance Premium Tax Return. Its significance is underscored by various aspects including the filing deadlines—August 15 and February 15, respectively, which hinge on the reporting period. Amendments or reports indicating no activity also form part of the filing options, emphasizing the form’s adaptability to different broker scenarios. Key details like the broker’s name, license number, and agency, along with the Minnesota Tax ID number, anchor the document's preliminary information, while calculations concerning premiums, fees, and taxes constitute its financial core. The legislation underpinning this process, notably the Nonadmitted and Reinsurance Reform Act (NRRA) of 2010, delineates tax liabilities relying on the insured’s "home state," streamlining tax payments to enhance compliance and efficiency in the surplus lines insurance market. Furthermore, detailed instructions accompany the IG260, offering clarity on completing the form, the requisite attachments, and payment modalities—whether electronic or check—to ensure accuracy and timeliness in submissions. This comprehensive approach underscores the form’s integral role in maintaining the alignment of surplus lines brokers with Minnesota’s regulatory framework and fiscal responsibilities.

*226341*

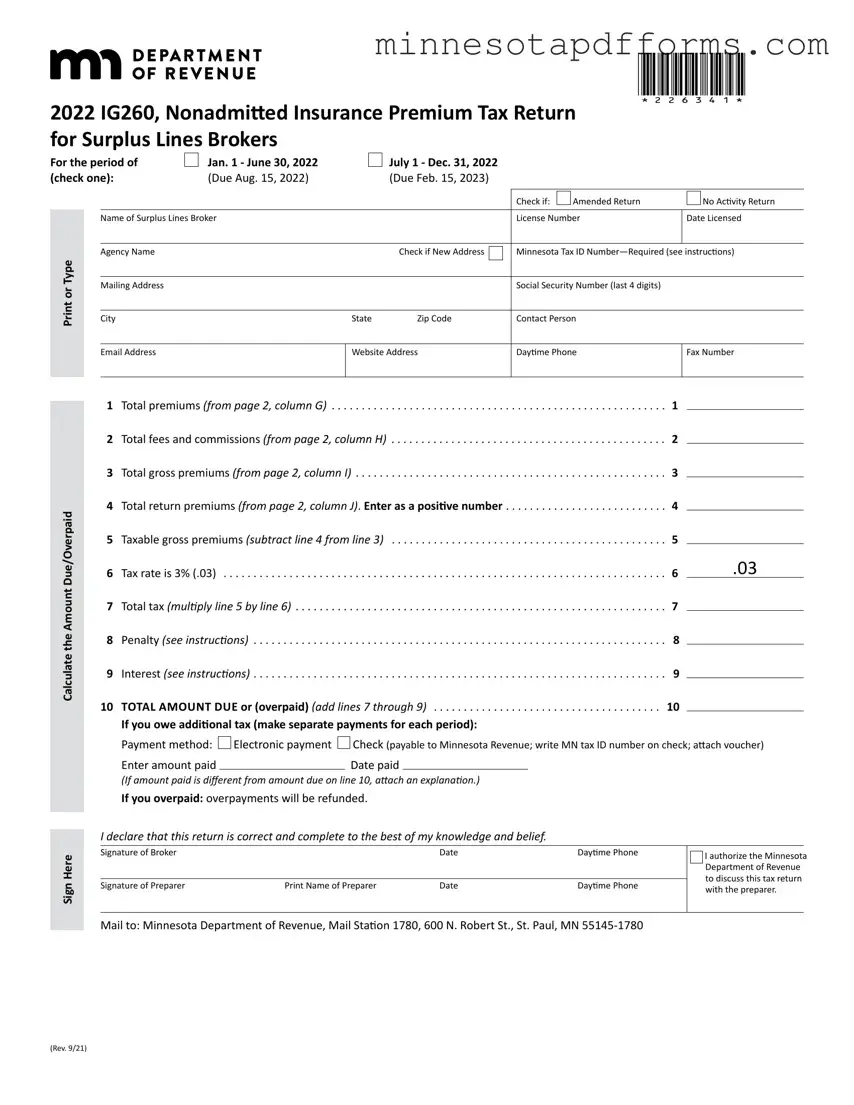

2022 IG260, Nonadmitted Insurance Premium Tax Return for Surplus Lines Brokers

For the period of (check one):

Jan. 1 - June 30, 2022

(Due Aug. 15, 2022)

July 1 - Dec. 31, 2022

(Due Feb. 15, 2023)

|

|

|

|

|

|

|

Check if: |

|

Amended Return |

|

No Activity Return |

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||

|

|

Name of Surplus Lines Broker |

|

|

|

|

License Number |

|

Date Licensed |

|||

|

|

|

|

|

|

|

|

|

||||

Type |

|

Agency Name |

|

Check if New Address |

|

|

Minnesota Tax ID |

|||||

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mailing Address |

|

|

|

|

Social Security Number (last 4 digits) |

|

|

|||||

or |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

State |

Zip Code |

|

|

Contact Person |

|

|

|||||

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

||||

|

|

Email Address |

Website Address |

|

|

Daytime Phone |

|

Fax Number |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Calculate the Amount Due/Overpaid

Sign Here

1 |

Total premiums (from page 2, column G) |

. . . |

. |

1. . |

. . . . . . . . . . . . . |

. . . |

2 |

Total fees and commissions (from page 2, column H) |

. . . . . |

. |

2 |

|

|

3 |

Total gross premiums (from page 2, column I) |

. . . |

. |

.3. |

. . . . . . . . . . . . . . |

. |

|

||||||

4 |

Total return premiums (from page 2, column J) . Enter as a positive number |

. . . |

. |

.4. |

. . . . . . . |

|

|

|

|||||

5 |

Taxable gross premiums (subtract line 4 from line 3) |

. . . . |

. |

5. . |

. . . . . . . . . . . |

|

6 |

Tax rate is 3% (.03) |

. . . . . |

6. . |

. . . . . . .03 |

|

|

|

|

|

|

|||

7 |

Total tax (multiply line 5 by line 6) |

. . . |

. |

.7 . |

. . . . . . . . . . . . . |

. . . . . |

|

||||||

8 |

Penalty (see instructions) |

. . |

. |

8. |

. . . . . . . . . . |

. . . . |

|

||||||

9 |

Interest (see instructions) |

. . |

. |

9. |

. . . . . . . . |

. . . . |

|

||||||

10 |

TOTAL AMOUNT DUE or (overpaid) (add lines 7 through 9) |

. . . . |

.10. . |

. . . . . |

|

|

|

|

|

||||

|

If you owe additional tax (make separate payments for each period): |

|

|

|

|

|

Payment method:  Electronic payment

Electronic payment  Check (payable to Minnesota Revenue; write MN tax ID number on check; attach voucher)

Check (payable to Minnesota Revenue; write MN tax ID number on check; attach voucher)

Enter amount paid |

|

Date paid |

(If amount paid is different from amount due on line 10, attach an explanation.)

If you overpaid: overpayments will be refunded.

I declare that this return is correct and complete to the best of my knowledge and belief.

|

|

|

|

|

|

|

|

|

Signature of Broker |

|

Date |

Daytime Phone |

|

|

I authorize the Minnesota |

||

|

|

|

||||||

|

|

|

|

|

|

Department of Revenue |

||

|

|

|

|

|

|

|||

|

|

|

|

|

|

to discuss this tax return |

||

Signature of Preparer |

Print Name of Preparer |

Date |

Daytime Phone |

|||||

|

|

with the preparer. |

||||||

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

Mail to: Minnesota Department of Revenue, Mail Station 1780, 600 N. Robert St., St. Paul, MN

(Rev. 9/21)

IG260

page 2

2022 Nonadmitted Insurance Premium Tax Return for Surplus Lines Brokers (continued)

A |

B |

C |

D |

E |

F |

G |

|

H |

I |

J |

NAIC |

|

|

Effective Date |

|

Trans |

Total |

. |

All Fees/ |

Total Gross |

Return |

Number |

Name of Insurer |

Policy Number |

(required) |

Name of Insured |

Type* |

Premiums |

|

Commissions |

Premiums (G + H) |

Premiums |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* See “Page 2, Column instructions” for a list of codes to enter in |

Subtotal (if more than one page) |

. . . |

|

|

|

||||

column F. |

Total. (Enter on appropriate lines on page 1) . . . . |

|

|

|

|

||||

|

|

|

|

||||||

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

2022 Form IG260 Instructions

For insurance tax laws, see Minnesota Statutes, Chapter 297I at www.leg.state.mn.us.

All surplus lines brokers that write or are authorized to write nonadmitted insurance must file Form IG260, Semiannual Statement of Surplus Lines Insurance, even if there is no activity or tax liability to report during the period. (M.S. 297I.05, subd. 7).

Filing Requirement

Effective July 21, 2011, the Nonadmitted and Reinsurance Reform Act of 2010 (NRRA) permits only the insured’s home state to require the payment of premium tax for nonadmitted insurance.

When Minnesota is the home state of the insured, as provided under M.S. 297I.05, subd. 7, 100% of the gross premiums are taxable in Minnesota with no allocation of the tax to other states.

“Home state” means the state in which an insured maintains its principal place of business, or in the case of an individual, the individual’s principal residence.

However, if 100% of the insured risk is located outside Minnesota, then the insured’s home state is the state to which the greatest percentage of the insured’s taxable premium for that insurance contract is allocated.

Minnesota Tax ID Required

Surplus lines insurance brokers are required to have their own Minnesota tax ID number. This is not a Social Security number or agency Minnesota tax ID number.

If you don’t have a Minnesota tax ID, you can apply online. Go to our website at www.revenue.state.mn.us and click “Register for a Minnesota tax ID number” on the e‑Services menu. Note: During the process, be sure to select “Sole proprietor” as the type of legal organization. Use

NAICS classification number 524210.

If you don’t have access to the Internet, call 651‑282‑5225 or 1‑800‑657‑3605 to register by phone.

Due Dates

File Form IG260 with all required attachments and pay any tax due by:

•Aug. 15 (for the six‑month period ending June 30)

•Feb. 15 of the following year (for the six‑month period ending Dec. 31) This form must be filed even if no tax is due for the period.

The U.S. postmark date, or date recorded or marked by a designated delivery service, is considered the filing date (private postage meter marks are not valid). When the due date falls on a Saturday, Sunday or legal holiday, returns and payments electronically made or postmarked on the next business day are considered timely. When a return or payment is late, the date it is received at the Department of Revenue is treated as the date filed or paid.

Extension for Filing Return. If good cause exists, you may request a filing extension.

Rules for Using Spreadsheets

If you are using your own spreadsheet, you must include all the information and in the same format as on page 2 of Form IG260, including subtotals on each page. Your filing will not be considered complete if all information, including subtotals, is not included.

If you have more than two pages of surplus lines insurance, submit an electronic file in addition to the printout. The files must be in a Microsoft Excel format.

Payments

Electronic Payments

If your total insurance taxes and surcharges for the last 12‑month period ending June 30 is $10,000 or more, you are required to pay your tax electronically in all subsequent years.

You must also pay electronically if you’re required to pay any Minnesota business tax electronically, such as withholding tax.

To pay over the Internet, go to the department’s website at www.revenue.state.mn.us and login. You’ll need your user name, password and bank routing and account numbers. When paying electronically, you must use an account that is not associated with any foreign banks.

If you use other electronic payment methods, such as ACH credit method or Fed Wire, instructions are available on our website or by calling our Business Registration Office at 651‑282‑5225 or 1‑800‑657‑3605.

Submit separate payments for each return.

Continued 1

2022 Form IG260 Instructions (continued)

Check Payments

If you’re not required to pay electronically and are paying by check, visit our website at www.revenue.state.mn.us and click on “Make a Payment” and then “By check” to create a voucher. Print and mail the voucher with a check made payable to Minnesota Revenue.

When you pay by check, your check authorizes us to make a one‑time electronic fund transfer from your account, and you may not receive your canceled check.

How to Complete the Form

Complete page 2 before page 1 of Form IG260.

Page 2, Column Instructions

A. NAIC Number

Enter the NAIC number.

B. Name of Insurer

List the insurers. Include policies for insurance companies without NAIC numbers.

C. Policy Number

The policy number (modified by the month and year that the policy was issued) is the controlling number for reporting surplus lines policies and any subsequent activity during the policy period, i.e., endorsements, audits and/or cancellations.

D. Effective Date (required)

Enter the effective date of the transaction.

E. Name of Insured

Provide the name of the insured.

F. Policy Transaction Type

Enter one of the following numbers:

1= New business 4 = Audit

2 = Renewal |

5 = Reinstatement |

3= Cancellation 6 = Endorsement

G. Total Premiums

Include all premiums paid by companies with a home state of Minnesota for risks located in the United States and U.S. territories.

H. Total Fees and Commissions (excluding stamping fee)

Include all fees and commissions paid by policyholder to obtain coverage that are not included in premiums.

I. Total Gross Premiums

Total premiums and all fees and commissions (column G plus column H).

J. Return Premiums

Enter all return premiums. Include a note indicating on which return the original policy was reported. Return premiums can only be claimed by the broker where the premiums and taxes were originally reported.

Page 1, Line Instructions

Check Boxes

At the top of the form, check if the return is:

•an Amended Return: Check only if you are amending a previously filed return for the same period. Include all original and corrected policies on the amended return.

•a No Activity Return: Check only if you did not have any activity during the period.

Line 4 — Total Return Premiums

Enter all return premiums as a positive number.

Line 5 — Taxable Gross Premiums

Gross premiums include fees and commissions.

Line 8 — Penalty

Late Payment. If you don’t pay all the tax due by the due date, a late payment penalty is due. The penalty is 5% of the unpaid tax for any part of the first 30 days the payment is late, and 5% for each additional 30‑day period, up to a maximum of 15%.

Continued 2

2022 Form IG260 Instructions (continued)

Late Filing. Add a late filing penalty to the late payment penalty if your return is not filed by the due date. The penalty is 5% of the unpaid tax. When added to the late payment penalty, the maximum combined penalty is 20%.

Payment Method. If you are required to pay electronically and do not, an additional 5% penalty applies to payments not made electronically, even if a paper check is sent on time.

Line 9 — Interest

You must pay interest on the unpaid tax plus penalty from the due date until the total is paid. The interest rate for calendar year 2022 is 3%. The interest rate may change for future years.

To figure how much interest you owe, use the following formula with the appropriate interest rate:

Interest = (tax + penalty) × # of days late × interest rate ÷ 365

Business Information Changes

Be sure to let us know within 30 days if you change mailing addresses, phone numbers, or any other business information. To do so, go to our website, login to e‑Services and update your profile information. By notifying us, we will be able to let you know of any changes in Minnesota tax laws and filing requirements.

Information and Assistance

Website: www.revenue.state.mn.us

Email: insurance.taxes@state.mn.us

Phone: 651‑556‑3024

This material is available in alternate formats.

For questions about licensing and regulations, contact the Minnesota Department of Commerce:

Website: www.mn.gov/commerce

Email: licensing.commerce@state.mn.us

Phone: 651‑539‑1599 or 1‑800‑657‑3978

Fax: 651‑539‑0107

For questions about stamping fees, contact the Surplus Lines Association of Minnesota (SLAM):

Website: www.mnsla.com

Email: nschroeder@mnsla.com

Phone: 320‑679‑4244

3

| Fact Name | Description |

|---|---|

| Purpose of Form IG260 | This form is used by surplus lines brokers in Minnesota to file Nonadmitted Insurance Premium Tax Returns, either for the first half or second half of the year. |

| Due Dates | Returns for the period of January 1 - June 30 are due by August 15, and returns for July 1 - December 31 are due by February 15 of the following year. |

| Governing Law | The form and its requirements are governed by Minnesota Statutes, Chapter 297I, specifically addressing taxation of insurance premiums and operations of surplus lines brokers. |

| Amended and No Activity Returns | Brokers can check specific boxes on the form to indicate whether they are filing an amended return or a return showing no activity for the reporting period. |

| Minnesota Tax ID Requirement | Surplus lines insurance brokers must have a Minnesota tax ID number to file Form IG260, separate from any Social Security number or agency Minnesota tax ID number. |

| Electronic Payments Requirement | If a broker's total insurance taxes and surcharges for the last 12-month period ending June 30 equals $10,000 or more, they are required to make payments electronically in subsequent years. |

Filling out the Minnesota IG260 form is a necessary step for surplus lines brokers in Minnesota to report nonadmitted insurance premium tax. This form is used both for regular reporting and to amend prior submissions or to file a return indicating no activity. The process involves providing detailed information about insurance transactions and calculating the total amount of tax due or overpaid. Below is a straightforward guide to completing the form accurately.

Remember to complete page 2 of form IG260 before starting on page 1, as page 2 will provide necessary details for the summary amounts on page 1. Keeping accurate and comprehensive records of all transactions will ensure that filling out the form is a smooth process. Should questions arise during this process, consult the contact information provided in the form instructions for assistance.

What is the purpose of the Minnesota IG260 form?

The Minnesota IG260 form, known as the Nonadmitted Insurance Premium Tax Return for Surplus Lines Brokers, is intended for surplus lines brokers to report and pay taxes on premiums collected for nonadmitted insurance policies. Nonadmitted insurance is provided by insurers that are not licensed to operate in Minnesota but are allowed to offer insurance under specific regulations.

Who is required to file Form IG260?

All surplus lines brokers licensed in Minnesota and authorized to write or have written nonadmitted insurance must file Form IG260. This requirement applies even if the broker did not engage in any taxable transactions or owe any taxes during the reporting period.

What periods does the IG260 cover, and when are the filings due?

For the period January 1 to June 30, the form is due by August 15.

For the period July 1 to December 31, the form is due by February 15 of the following year.

If the due date falls on a weekend or a legal holiday, the form and any payment are deemed timely if submitted on the next business days.

Are there penalties for late filing or payment?

Yes, penalties apply for late filings and payments. A late payment penalty is 5% of the unpaid tax for any part of the first 30 days overdue, with an additional 5% for each subsequent 30-day period, up to a 15% maximum. A late filing penalty, assessed in addition to the late payment penalty, is 5% of the unpaid tax, making the combined maximum penalty 20%. An extra 5% penalty is added for failing to pay electronically when required.

How are payments made for the tax due on the IG260 form?

Payments can be made electronically via the department’s website or by phone. If you're not required to pay electronically and prefer to pay by check, a voucher must be created online to accompany your check payment.

What should I do if I need to amend a previously filed IG260 form?

To amend a previously filed IG260, mark the "Amended Return" box on the form. Include all originally reported policies and any corrections in your amended return.

How do surplus lines brokers obtain a Minnesota tax ID number?

Surplus lines brokers must have a specific Minnesota tax ID number, which can be obtained by registering online through the Minnesota Department of Revenue website. During the registration process, select “Sole proprietor” as the type of legal organization and use the NAICS classification number 524210 for surplus lines brokerage activities.

What if there was no activity during the reporting period?

Brokers must file a "No Activity Return" by checking the appropriate box on the IG260 form if no taxable transactions occurred during the period.

Where can surplus lines brokers find assistance for completing the IG260 form or any related inquiries?

Assistance is available through the Minnesota Department of Revenue’s website and customer service numbers. For licensing and regulations, the Minnesota Department of Commerce provides resources. The Surplex Lines Association of Minnesota (SLAM) offers guidance on stamping fees and industry-specific queries.

Not obtaining or correctly entering the Minnesota Tax ID number: Every surplus lines broker must have their own Minnesota tax ID number, distinct from their Social Security number or agency tax ID. This number is crucial for identifying the broker in the state's tax system, and failing to obtain or correctly enter it on the form can lead to processing delays.

Incorrectly classifying the type of period covered: The form requires brokers to indicate whether the report covers the period from January 1 to June 30 or from July 1 to December 31. Failing to check one of these boxes or checking the wrong one can lead to confusion and inaccuracies in tax liability assessment.

Forgetting to check if the return is amended or reports no activity: If a broker is submitting an amended return or if there has been no activity in the reporting period, specific boxes must be checked. Ignoring these options might result in incorrect processing of the return.

Misreporting total premiums, fees, and commissions: Accurately reporting total premiums from page 2, column G, and total fees and commissions from page 2, column H, is critical. These figures are essential for determining the correct tax liability. Misreporting these figures can lead to an incorrect calculation of the tax due.

Failure to accurately calculate taxable gross premiums: Taxable gross premiums are determined by subtracting total return premiums from the total gross premiums. Incorrect calculations in this step will directly affect the tax amount owed.

Omitting penalty or interest owed if applicable: If the tax payment is late, the form requires the addition of penalties and interest. Failing to include these amounts when applicable can result in underpayment of the tax owed and further penalties.

Incorrect use of electronic or check payments: Brokers with a tax liability of $10,000 or more in the past 12 months are required to pay electronically. Incorrect payment methods such as sending a check when electronic payment is mandated can result in penalties. Similarly, when paying by check, not following the correct procedure for check payments, such as failing to attach a payment voucher, can cause processing issues.

When completing the Minnesota IG260 form, accuracy and attention to these details are instrumental in ensuring compliance with the state’s tax requirements for surplus lines brokers. Overlooking these common mistakes can lead to processing delays, inaccurate tax liability calculations, and potential penalties.

When dealing with the Minnesota IG260 form, which is a Nonadmitted Insurance Premium Tax Return for Surplus Lines Brokers, it’s important to recognize that this form doesn't exist in isolation. Various documents often accompany it, aimed at providing comprehensive reporting and compliance with the Minnesota Department of Revenue. Let’s explore a few of these ancillary forms and documents that are typically used alongside the IG260 form.

The IG260 form, coupled with these documents, ensures a well-documented and compliant submission to the Minnesota Department of Revenue. It's advisable for surplus lines brokers to familiarize themselves with these documents to streamline their tax reporting processes and maintain compliance with state regulations.

The Minnesota IG260 form, used for Nonadmitted Insurance Premium Tax Returns by Surplus Lines Brokers, shares similarities with the NAIC Quarterly Statement that insurance companies must file. Like the IG260, this quarterly statement requires detailed accounting of premiums collected, adjustments, and taxes due. Both documents are crucial for regulatory compliance, ensuring that insurers and brokers accurately report their financials to state regulators. Additionally, they both demand meticulous record-keepings, such as total premiums and returns, and are essential tools for financial transparency within the insurance industry.

Another document resembling the IG260 form is the IRS Form 720, Quarterly Federal Excise Tax Return. Both forms involve the reporting and payment of taxes, albeit for different purposes and jurisdictions. Form 720 captures excise taxes on specific goods, services, and activities, whereas IG260 focuses on the premium tax related to surplus lines insurance. Despite their focused differences, each form plays a pivotal role in fulfilling tax obligations, requiring filers to calculate taxes due and accompanying penalties for late payments, if applicable.

The Uniform Application for State Insurance License/Registration (NIPR) also bears resemblance to the IG260 form in its function for brokers and agents. While the IG260 deals with the tax reporting aspects of surplus lines brokerage, the NIPR application is essential for individuals seeking authorization to operate as licensed insurance professionals. Both documents necessitate accurate personal and business information, licensure details, and regulatory compliance, yet they serve different procedural needs within the insurance sector's regulatory framework.

Lastly, the Surplus Lines Association Electronic Filing System (SLA EFS) submissions are akin to the IG260 form, especially for those brokers dealing with surplus lines in states requiring SLA membership. Similar to IG260's role in tax reporting, SLA EFS submissions ensure compliance with state-specific reporting requirements for surplus lines transactions. Both require detailed transaction records, including premiums and the tax rates applied, underscoring the importance of precise accounting and regulatory adherence in the insurance domain.

When completing the Minnesota IG260 form for Nonadmitted Insurance Premium Tax Returns for Surplus Lines Brokers, paying close attention to the details is crucial. Here are 10 dos and don'ts to help guide you through the process:

Do:

Don't:

By following these guidelines, you can ensure a smoother process and avoid common pitfalls when submitting your Minnesota IG260 form.

When dealing with the Minnesota IG260 form, a form used for reporting Nonadmitted Insurance Premium Tax Returns by Surplus Lines Brokers, several misconceptions can complicate its filing. Understanding these misconceptions can help ensure accurate and timely submissions.

Ensuring an accurate understanding of these misconceptions around the Minnesota IG260 form can help surplus lines brokers comply more effectively with the state's regulatory requirements, thus avoiding unnecessary penalties or delays.

When completing the Minnesota IG260 form, which is used for reporting Nonadmitted Insurance Premium Tax Return for Surplus Lines Brokers, it's important to grasp these key takeaways:

Understanding these aspects of the IG260 form brings clarity and ease to the filing process, ensuring that surplus lines brokers can fulfill their tax obligations efficiently and accurately.

Minnesota Sales and Use Tax - Identify the extent of your business’s sales tax nexus in Minnesota with form ST101 and ensure compliance with state regulations.

Dhs 7823 - Cover sheet for compiling key service recipient information, ensuring easy access to important details.