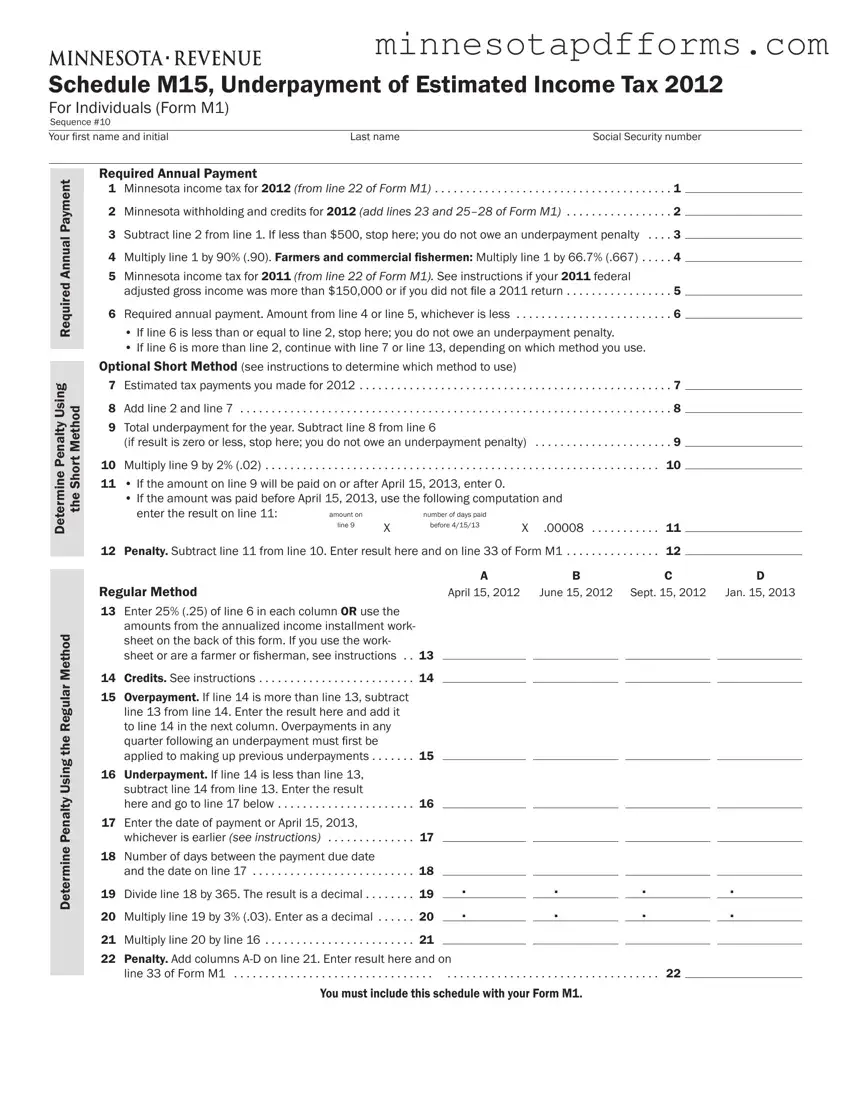

Required Annual Payment

1 Minnesota income tax for 2012 (FROM LINE 22 OF FORM M1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Minnesota withholding and credits for 2012 (ADD LINES 23 AND 25–28 OF FORM M1) . . . . . . . . . . . . . . . . . 2

3 Subtract line 2 from line 1. If less than $500, stop here; you do not owe an underpayment penalty . . . . 3

4 Multiply line 1 by 90% (.90). Farmers and commercial ishermen: Multiply line 1 by 66.7% (.667) . . . . . 4

5Minnesota income tax for 2011 (FROM LINE 22 OF FORM M1). See instructions if your 2011 federal

adjusted gross income was more than $150,000 or if you did not ile a 2011 return . . . . . . . . . . . . . . . . . 5

6 Required annual payment. Amount from line 4 or line 5, whichever is less . . . . . . . . . . . . . . . . . . . . . . . . . 6

•If line 6 is less than or equal to line 2, stop here; you do not owe an underpayment penalty.

•If line 6 is more than line 2, continue with line 7 or line 13, depending on which method you use.

Optional Short Method (see instructions to determine which method to use)

7 Estimated tax payments you made for 2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

8 Add line 2 and line 7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

9 Total underpayment for the year. Subtract line 8 from line 6 |

|

(if result is zero or less, stop here; you do not owe an underpayment penalty) |

9 |

10 Multiply line 9 by 2% (.02) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11• If the amount on line 9 will be paid on or after April 15, 2013, enter 0.

• If the amount was paid before April 15, 2013, use the following computation and

enter the result on line 11: |

amount on |

|

number of days paid |

|

|

|

|

|

line 9 |

X |

before 4/15/13 |

X .00008 |

. . . . . 11 |

|

|

12 Penalty. Subtract line 11 from line 10. Enter result here and on line 33 of Form M1 |

. . . . . 12 |

|

|

|

|

|

A |

B |

C |

D |

Regular Method |

|

|

April 15, 2012 |

June 15, 2012 |

Sept. 15, 2012 |

Jan. 15, 2013 |

13Enter 25% (.25) of line 6 in each column OR use the amounts from the annualized income installment work-

sheet on the back of this form. If you use the work-

sheet or are a farmer or isherman, see instructions . . 13

14 Credits. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . 14

15Overpayment. If line 14 is more than line 13, subtract line 13 from line 14. Enter the result here and add it

to line 14 in the next column. Overpayments in any quarter following an underpayment must irst be

applied to making up previous underpayments . . . . . . . 15

16Underpayment. If line 14 is less than line 13, subtract line 14 from line 13. Enter the result

here and go to line 17 below . . . . . . . . . . . . . . . . . . . . . . 16

17Enter the date of payment or April 15, 2013,

whichever is earlier (SEE INSTRUCTIONS) . . . . . . . . . . . . . . 17

18Number of days between the payment due date

|

and the date on line 17 |

18 |

|

|

|

|

|

|

|

19 |

Divide line 18 by 365. The result is a decimal |

19 |

. |

|

. |

|

. |

|

. |

20 |

Multiply line 19 by 3% (.03). Enter as a decimal |

20 |

. |

|

. |

|

. |

|

. |

21 Multiply line 20 by line 16 . . . . . . . . . . . . . . . . . . . . . . . . 21

22Penalty. Add columns A-D on line 21. Enter result here and on

line 33 of Form M1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22