Free Minnesota M30 Template

Free Minnesota M30 Template

The Minnesota M30 form serves as a critical document for companies operating within the state, focusing on the computation and reporting of the occupation tax. This comprehensive form requires detailed financial information, including gross income, production costs, and an array of deductions such as salaries, repairs, and depreciation, aimed at calculating the company's net income and, subsequently, its tax liability. Additionally, the form provides for adjustments related to endangered resource donations, payments extending from the previous year, and penalties or interest applicable to the reporting period. As part of the submission process, companies are tasked with disclosing any ongoing or finalized federal examinations, a step that ensures the state's revenue service has the most accurate and up-to-date information. Amendments to the initially reported tax are facilitated through the Form M30X, highlighting the form's adaptive framework in response to post-submission audits or recalculations. Further complexities are introduced with attachments that guide the tax apportionment based on the company's operational scope within and outside Minnesota, alongside the calculation of net income adjustments and the determination of applicable credits. This rigorous documentation process not only embodies Minnesota's efforts to ensure a fair tax system but also underscores the intricate relationship between state tax obligations and federal tax compliance.

M30

2005 Occupation Tax

Print or type

Tax, payments and credits

Amount due or overpaid

Sign here

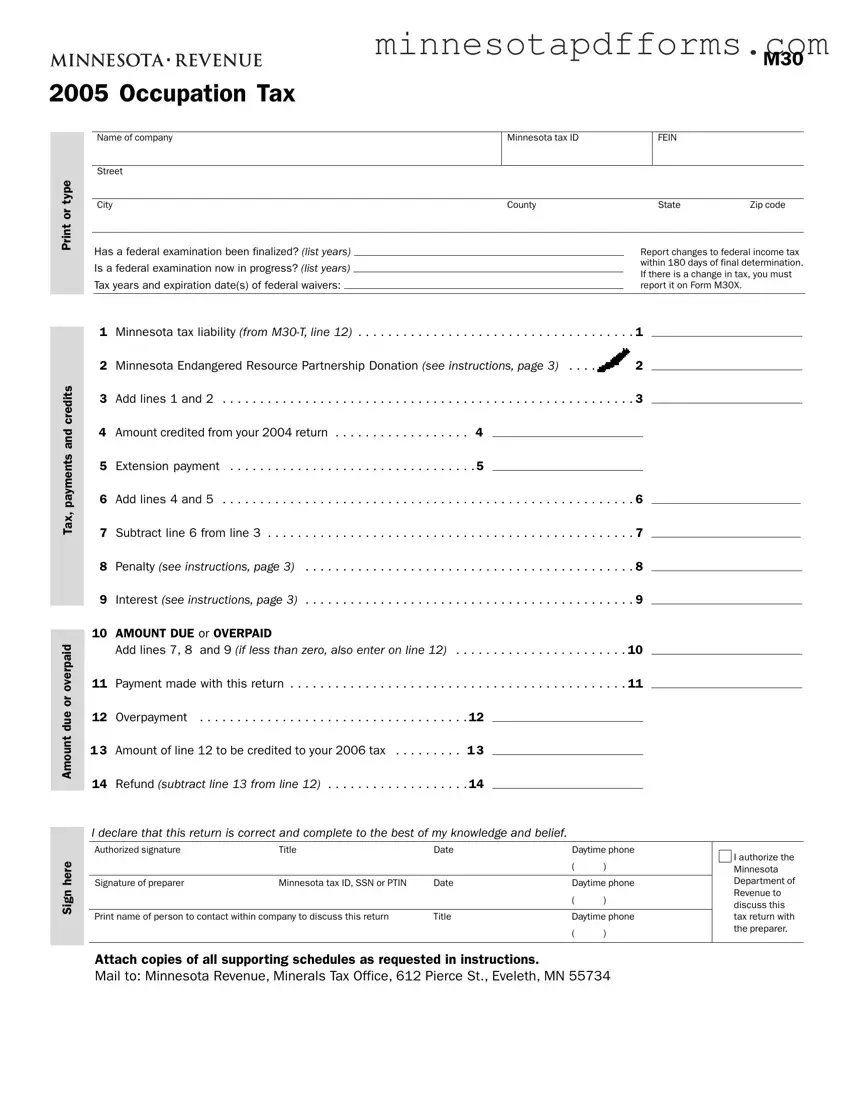

Name of company |

Minnesota tax ID |

FEIN |

|

|

|

|

|

Street |

|

|

|

|

|

|

|

City |

County |

State |

Zip code |

Has a federal examination been finalized? (list years) |

|

Report changes to federal income tax |

||

Is a federal examination now in progress? (list years) |

|

|

within 180 days of final determination. |

|

|

|

If there is a change in tax, you must |

||

|

|

|

|

|

Tax years and expiration date(s) of federal waivers: |

|

|

report it on Form M30X. |

|

|

|

|

|

|

1 |

Minnesota tax liability (from |

. . . |

. . . . . . . . . . . . . . . . . . |

. 1 |

2 |

Minnesota Endangered Resource Partnership Donation (see instructions, page 3) . . . . |

2 |

||

3 |

Add lines 1 and 2 |

. . . . . . . . . . . . . . . . . . |

. 3 |

|

4 |

Amount credited from your 2004 return |

4 |

|

|

5 |

. .Extension payment |

. 5 |

|

|

6 |

Add lines 4 and 5 |

. . . . . . . . . . . . . . . . . . |

. 6 |

|

7 |

Subtract line 6 from line 3 |

. . . . . . . . . . . . . . . . . . |

. 7 |

|

8 |

Penalty (see instructions, page 3) |

. . . |

. . . . . . . . . . . . . . . . . . |

. 8 |

9 |

Interest (see instructions, page 3) |

. . . |

. . . . . . . . . . . . . . . . . . |

. 9 |

10 |

AMOUNT DUE or OVERPAID |

|

|

|

|

Add lines 7, 8 and 9 (if less than zero, also enter on line 12) . . |

. . . |

. . . . . . . . . . . . . . . . . . |

10 |

11 |

Payment made with this return |

. . . |

. . . . . . . . . . . . . . . . . . |

11 |

12 |

Overpayment |

12 |

|

|

1 3 |

. .Amount of line 12 to be credited to your 2006 tax |

1 3 |

|

|

14 |

. . .Refund (subtract line 13 from line 12) |

14 |

|

|

I declare that this return is correct and complete to the best of my knowledge and belief.

Authorized signature |

Title |

Date |

Daytime phone |

I authorize the |

|

|

|

|

|

|

|

|

|

|

( |

) |

Minnesota |

|

|

|

|

|

|

Signature of preparer |

Minnesota tax ID, SSN or PTIN |

Date |

Daytime phone |

Department of |

|

|

|

|

( |

) |

Revenue to |

|

|

|

discuss this |

||

|

|

|

|

|

|

Print name of person to contact within company to discuss this return |

Title |

Daytime phone |

tax return with |

||

|

|

|

( |

) |

the preparer. |

|

|

|

|

||

|

|

|

|

|

|

Attach copies of all supporting schedules as requested in instructions.

Mail to: Minnesota Revenue, Minerals Tax Office, 612 Pierce St., Eveleth, MN 55734

2005 Income Calculation

Attachment #1

Name of company

Minnesota tax ID

FEIN

Income

Deductions

1 Gross income (from

2 Cost of pellets produced (from Schedule A, line 8) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

3 |

Gross profit (subtract line 2 from line 1) |

. . . . |

. . . . . . . . . . . . . . . . . . |

3 |

4 |

Net gain or loss (see instructions) |

. . . . |

. . . . . . . . . . . . . . . . . . |

4 |

5 |

Other adjustments (see instructions) |

. . . . |

. . . . . . . . . . . . . . . . . . |

5 |

6 |

Total income (add lines 3, 4 and 5) |

. . . . |

. . . . . . . . . . . . . . . . . . |

6 |

7 |

Salaries and wages |

. . . . |

. . . . . . . . . . . . . . . . |

7. . . . |

8 |

Repairs |

. . . . |

. . . . . . . . . . . . . . . . |

8. . . . |

9 |

Rents and leases |

. . . . |

. . . . . . . . . . . . . . . . |

9. . . . |

10 |

Royalties |

. . . . |

. . . . . . . . . . . . . . . . |

10. . . |

11 |

Taxes |

. . . . |

. . . . . . . . . . . . . . . . |

11. . . |

12 |

Interest |

. . . . |

. . . . . . . . . . . . . . . . |

12. . . |

13 |

Depreciation (see instructions) |

13 |

|

|

14 |

Less depreciation on Schedule A or elsewhere on return |

14a |

|

14b |

1 5 |

Eighty percent of federal bonus depreciation |

. . . . |

. . . . . . . . . . . . . . . . |

1 5. . . |

1 6 |

Subtraction for prior bonus depreciation addback |

. . . . |

. . . . . . . . . . . . . . . . |

1 6. . . |

17 |

Development |

. . . . |

. . . . . . . . . . . . . . . . |

17. . . |

18 |

Depletion (see instructions) |

. . . . |

. . . . . . . . . . . . . . . . . . |

18. . . |

19 |

Pension, |

. . . . |

. . . . . . . . . . . . . . . . |

19. . . |

20 |

Employee benefit programs |

. . . . |

. . . . . . . . . . . . . . . . |

20. . . |

21 |

Other deductions |

. . . . |

. . . . . . . . . . . . . . . . |

21. . . |

22 |

Total deductions (add lines 7 through 21) |

. . . . |

. . . . . . . . . . . . . . . . . . |

22. . . |

23 |

Minnesota net income (loss) (subtract line 22 from line 6) |

. . . . |

. . . . . . . . . . . . . . . . . . |

23. . . |

|

Enter on |

|

|

|

2005 Apportionment

Name of company |

Minnesota tax ID |

|

|

A

Total in and

outside Minnesota

1 Average inventory . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2Average tangible property and

|

|

land owned/used (at original cost) |

2 |

|

ratio |

3 |

Capitalized rents (gross rents x 8) |

3 |

|

|

|

|

|

|

Property |

4 |

Total property (add lines 1 – 3) |

4 |

|

|

5 |

Percentage within Minnesota |

|

|

|

|

(see instructions, page 6 ) |

. .5 |

|

6 Factor weight . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

7 Weighted ratio for PROPERTY (multiply line 5 by line 6) . . . . . . . . . . . . . . . . . . . . . . . 7

8 Payroll/officer’s compensation . . . . . . . . . . . . . . . . . . . 8

9Percentage within Minnesota

ratio |

|

|

(see instructions, page 6) |

. . . .9 |

||

|

|

|

||||

Payroll |

10 |

Factor weight |

. . . .10 |

|||

|

||||||

|

11 |

Weighted ratio for PAYROLL (multiply line 9 by line 10) . |

. . . .11 |

|||

|

12 |

Sales or gross receipts |

12 |

|

||

ratio |

|

|||||

13 |

Percentage within Minnesota (see instructions, page 6 ) |

. . .13 |

||||

|

||||||

Sales |

14 |

Factor weight |

. . .14 |

|||

|

||||||

|

15 |

Weighted ratio for SALES (multiply line 13 by line 14) . . . |

. . .15 |

|||

|

|

16 |

APPORTIONMENT FACTOR (add lines 7, 11 and 15 ) . |

. . .16 |

||

|

|

|||||

|

|

|

Enter on |

|

|

|

Attachment #4

FEIN

B

In Minnesota

0.125

0.125

0.75

2005 Tax Calculation

Attachment #5

Name of company

Minnesota tax ID

FEIN

Income and deductions

Tax, credits and liability

1 |

Minnesota net income (from |

. 1 |

2 |

Apportionment factor (from |

. 2 |

3 |

Net income apportioned to Minnesota (multiply line 1 by line 2) |

. 3 |

4 |

Net operating loss deduction (from |

. 4 |

5 |

Taxable income (subtract line 4 from line 3; if zero or less, enter zero) |

. 5 |

6 |

Regular tax (multiply line 5 by 9.8% [.098]) |

. 6 |

7 |

Alternative minimum tax (from |

. 7 |

8 |

Add lines 6 and 7 |

. 8 |

9 |

AMT credit (from |

. 9 |

10 |

Subtract line 9 from line 8 |

10 |

11 |

Minnesota research credit (from |

11 |

12 |

Subtract line 11 from line 10. This is your MINNESOTA TAX LIABILITY |

12 |

|

Enter on M30, line 1. |

|

| Fact | Description |

|---|---|

| Form Title | Minnesota M30 Occupation Tax Form |

| Governing Law | Minnesota State Law |

| Purpose | To calculate and report the occupation tax due by companies operating within Minnesota |

| Submission Requirement | Must be filed by companies with Minnesota tax liability |

| Key Sections | Tax, payments and credits; Amount due or overpaid; Signature section |

| Adjustments | Adjustments for federal examination changes and federal waivers reported via Form M30X |

| Attachments | Income Calculation (M30-I), Apportionment (M30-A), and Tax Calculation (M30-T) along with other supporting schedules |

| Donation Option | Minnesota Endangered Resource Partnership Donation |

| Mailing Address | Minnesota Revenue, Minerals Tax Office, 612 Pierce St., Eveleth, MN 55734 |

Filling out the Minnesota M30 form is an important task for companies operating within the state, as it pertains to the occupation tax that must be accurately reported to comply with state tax laws. This process can seem daunting, but breaking it down into manageable steps can simplify the task. Once the form is correctly filled out and submitted, the company remains in good standing regarding its tax obligations, ensuring that all financial and taxation records are in line with state requirements. The following steps delineate how to complete the M30 form.

By following these detailed steps, companies can ensure that they accurately complete and submit their Minnesota M30 form, adhering to the state's tax reporting obligations. This procedure, though intricate, is crucial for maintaining compliance and supporting Minnesota’s tax infrastructure.

What is the Minnesota M30 form used for?

The Minnesota M30 form is utilized for reporting and calculating the occupation tax that companies engaged in certain industries owe to the state of Minnesota. This form helps businesses determine their tax liability based on their net income apportioned to Minnesota, adjusted by various factors such as deductions, credits, and specific adjustments related to the tax year in question.

Who needs to file the Minnesota M30 form?

The M30 form is mandatory for companies operating within specific sectors that are subject to Minnesota's occupation tax. This primarily includes businesses involved in the extraction, production, or exploitation of natural resources within the state. To understand fully if your business falls under this requirement, it's advisable to check the latest guidelines provided by the Minnesota Department of Revenue.

When is the M30 form due?

Like many tax forms, the M30 must be filed on an annual basis. The specific due date can vary from year to year, so it's crucial to consult the Minnesota Department of Revenue's calendar for the exact deadlines. Generally, companies are expected to submit their M30 form and any payment due by the established due date to avoid penalties and interest.

What should be included when you file the M30 form?

When filing the M30, it's important to include all required information such as the company's name, Minnesota tax ID, FEIN, contact information, and comprehensive financial data that accurately reflects the business's tax liability. Additionally, supporting schedules and documents that detail income, deductions, apportionment factors, and credits must be attached to ensure the form is processed correctly.

What happens if there is a change in tax after a federal examination?

If a federal examination results in a change to your income tax that affects your occupation tax, you are required to report this adjustment to the Minnesota Department of Revenue. This should be done using the Form M30X, and it must be filed within 180 days of the federal determination to ensure your tax records are accurate and up-to-date.

How do you calculate the Minnesota tax liability on the M30 form?

Calculating the Minnesota tax liability involves several steps outlined in the M30 form instructions. First, you need to determine your Minnesota net income from the M30-I attachment. Then, apply the apportionment factor from the M30-A attachment to identify the portion of income attributable to Minnesota. Following this, deductions such as net operating losses are subtracted, after which the regular and alternative minimum taxes are calculated and summed. This final amount, adjusted by available credits, represents your Minnesota tax liability.

Can you make a donation through the M30 form?

Yes, companies filing the M30 form have the option to contribute to the Minnesota Endangered Resource Partnership. This donation is made by filling in the appropriate section on the form and will be added to the total tax liability or deducted from any refund owed to the company.

What are the penalties for late filing or payment?

Companies that submit their M30 form or payment after the due date may face penalties and interest. These charges are calculated based on the amount of tax due and the length of the delay. It's essential to file and pay on time to avoid these additional costs, and if necessary, companies can apply for an extension to prepare their documentation adequately.

Where should the completed M30 form be sent?

The completed M30 form, along with any supporting documentation and payment, should be mailed to the Minnesota Revenue, Minerals Tax Office, located at 612 Pierce St., Eveleth, MN 55734. Ensuring that all parts of the form are filled out correctly and that all necessary attachments are included will help avoid processing delays.

Filling out the Minnesota M30 form correctly is crucial for companies to ensure accuracy in reporting their taxes. However, errors can occur, leading to potential issues with the Minnesota Department of Revenue. Below are nine common mistakes people make when filling out this form:

In addition to these specific mistakes:

Ensouring accuracy and completeness when filling out the Minnesota M30 form is paramount. Small mistakes can lead to large discrepancies, potentially resulting in audits, fines, or penalties. Companies are advised to carefully review their submissions and consider seeking professional assistance if they are uncertain about the form's requirements.

When preparing and filing the Minnesota M30 form, which is used for calculating occupation tax, companies are often required to submit additional forms and documents to support their tax calculations and substantiate claims made on the primary form. Understanding these supplementary documents can help ensure compliance and accuracy in tax reporting.

Comprehensively understanding and accurately completing these forms and schedules are essential aspects of fulfilling Minnesota's occupation tax requirements. Each document plays a crucial role in the calculation and verification process, ensuring that companies accurately report their tax liabilities and claim entitlements. Seek professional advice if you're uncertain about how to properly complete these forms, as accurate reporting benefits all parties involved.

The Minnesota M30 form, in its essence, functions similarly to the U.S. Corporation Income Tax Return (IRS Form 1120). Both forms require detailed financial information from companies, including gross income, deductions, and net income. While the IRS Form 1120 is for federal tax purposes, the Minnesota M30 serves the state's tax obligations, focusing particularly on the occupation tax. The requirement to list income, deductions, and calculate tax liability based on this information is a uniform aspect between them, making the M30 a state-level counterpart to the federal form.

Another comparable document is the Schedule K-1 (Form 1065), which is used for reporting the share of income, deductions, credits, etc., of each partner of a partnership. Like the M30's sections that require detailing income and deductions to determine tax liability, Schedule K-1 deals with allocating these figures among partners. However, the M30 focuses on the company as a single entity, while Schedule K-1 distributes financial details among individuals or entities in a partnership.

The Minnesota M30 also shares similarities with the State Business Tax Return forms that are filed in other states. While each state has its own name and specific requirements for their business tax forms, they all serve the purpose of calculating state tax liability based on income, similar to the M30. These forms, like the M30, include spaces for reporting income, deductions, tax credits, and payments. The primary difference lies in state-specific tax rates, credits, and exemptions.The U.S. Return of Partnership Income (IRS Form 1065) also parallels the M30 in its structure of income and deduction reporting. While Form 1065 is for partnerships at the federal level, detailing operational financial activities, the M30 accomplishes a similar task for individual corporations on the state level in Minnesota, aiming to ascertain the appropriate occupation tax.

Form M30X, referred to in the M30 instructions for reporting changes in tax due to federal adjustments, is conceptually similar to the IRS Form 1040X, which is the Amended U.S. Individual Income Tax Return. Both forms are designed to correct or update previous submissions, whether it be for an individual or a corporation. The necessity for such forms arises from the inevitability of amendments to previously filed returns due to errors, omissions, or changes following federal audits.

The Alternative Minimum Tax form for corporations (IRS Form 4626) is another document sharing a conceptual bond with parts of the M30. Similar to the M30's section on alternative minimum tax, Form 4626 is used at the federal level to calculate this tax for corporations, ensuring that they pay at least a minimum amount of tax if they benefit excessively from certain deductions and credits. Both documents ensure entities contribute a fair share of taxes, preventing overuse of tax benefits.

Lastly, the M30's requirement for companies to report adjustments following a federal examination mirrors the function of the IRS Form 5471, Information Return of U.T.S. Persons With Respect to Certain Foreign Corporations. Though Form 5471 is more specific in scope, focusing on foreign corporations, the underlying purpose of reporting changes in tax liability due to adjustments—whether international or domestic—draws a parallel between these documents. Both forms ensure that tax obligations reflect the accurate financial position post-audit or examination.

When filling out the Minnesota M30 form, there are several practices you should follow to ensure accuracy and compliance. Below, you'll find lists of what you should and shouldn't do during the process.

Things you should do:

Things you shouldn't do:

When discussing the Minnesota M30 form, there are several misconceptions that can lead to confusion. Understanding the reality behind these misconceptions can help individuals and companies navigate their tax responsibilities more effectively.

Many believe that the M30 form's sole purpose is to report income. However, it encompasses much more, including tax liabilities, deductions, credits, and details about conservation efforts through the Minnesota Endangered Resource Partnership Donation. It requires a comprehensive report of the taxpayer's financial activities, not just income.

Another common misunderstanding is that changes cannot be reported after the initial submission. In contrast, the form instructs taxpayers to report changes to federal income tax within 180 days of a final determination, using Form M30X for corrections, highlighting the process for amending previously reported information.

It's often thought that the M30 form solely focuses on the current year's financial data. However, it also inquires about federal examinations for previous years and tracks carryforward amounts like overpayments to be credited or refunded. This shows the necessity to maintain and provide historical financial data.

There's a belief that the M30 form strictly deals with the Minnesota-specific operations of a business. Yet, it includes sections for apportionment factors that account for a company's activities both in and outside Minnesota, indicating a broader evaluation of the company's operations and its allocation for state tax purposes.

Understanding these misconceptions is crucial for accurate and compliant tax reporting. Companies must look beyond these myths to grasp the full extent of their reporting obligations under the M30 form.

Filling out the Minnesota M30 form requires a careful understanding of your company's financial activities within the state. Here are some key takeaways to help guide you through this process:

Properly completing the M30 form requires attention to detail and understanding of your company's financial standing in Minnesota. By following each step carefully and consulting the instructions provided, you can ensure compliance and minimize the risk of errors in your tax filing.

Minnesota Repossession Laws - Allows for the formal declaration of vehicle repossession in Minnesota, setting the stage for a new title application.

Mn Permit to Carry Disqualifications - The form's detailed nature ensures only qualified individuals can purchase or transfer firearms, thereby regulating ownership responsibly.

Mncred - Details of the primary or pending practice location, including practice type and new patient acceptance, are required.