Free Minnesota M4Np Template

Free Minnesota M4Np Template

In the landscape of tax documentation and procedures, the Minnesota M4NP form plays a crucial role for tax-exempt organizations and cooperatives that file federal Form 990-T or 1120-C, striking a fine balance between regulatory compliance and financial efficiency. This specific document is designed to meticulously track and apply net operating losses (NOLs), thereby offering a means to manage and potentially reduce taxable income over time. The form entails an in-depth outline for reporting the organization's Minnesota taxable net income or losses, alongside a detailed record of how losses have been utilized or carried forward in subsequent years. Noteworthy is the form's adaptation to changes in tax law, specifically the transition to carry forward only provisions for NOLs, eliminating the option to carry back losses to previous tax years for those beginning after December 31, 2017. Furthermore, it limits the deduction of NOLs to 80% of the taxable net income for the year, emphasizing a forward-looking strategy in loss management over a span of 15 years. The necessity for separate M4NP NOL schedules for each entity within a unitary group underlines the complexity and precision required in navigating the form's directives. Despite its detailed instructions and constraints, such as the prohibition for organizations filing under federal Form 1120-H or 1120-POL to claim NOL deductions, this document stands as a testament to the intricate interplay between tax regulation and organizational fiscal stewardship.

*226651*

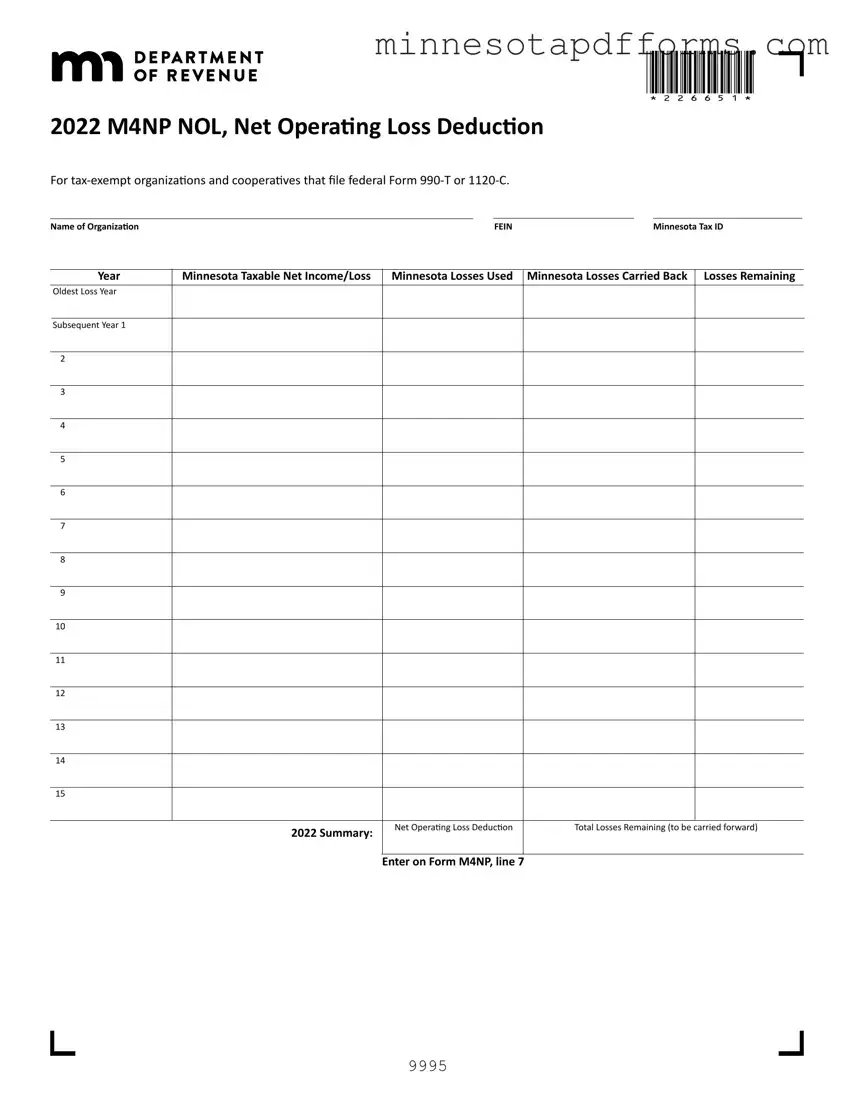

2022 M4NP NOL, Net Operating Loss Deduction

For

Name of OrganizationFEINMinnesota Tax ID

Year |

Minnesota Taxable Net Income/Loss |

Minnesota Losses Used Minnesota Losses Carried Back Losses Remaining |

Oldest Loss Year

Subsequent Year 1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

2022 Summary: |

Net Operating Loss Deduction |

Total Losses Remaining (to be carried forward) |

|

|

Enter on Form M4NP, line 7

9995

2022 Schedule M4NP NOL Instructions

Use this form to show the sources and applications of your net operating losses. List the years you used to calculate the net operating loss and the years you used the losses.

Your net operating loss deduction is limited to 80% (0.80) of your taxable net income for the year. Net operating losses may be carried forward only. The carry forward period is 15 years.

Starting with tax years beginning after December 31, 2017, the

You may deduct a net operating loss incurred in a prior year and not previously used to offset net income on Form M4NP, Unrelated Business Income Tax Return, line 7.

If you conduct your business entirely in Minnesota, you may deduct the full amount of any previously unused net operating loss after the 80%

limitation is applied.

If you apportion your income to Minnesota, you may deduct any previously unused net operating loss at the apportionment percentage of the

loss year.

You may not create or increase the net operating loss by the:

•Deduction for dividends received

•Foreign royalties subtraction for tax years beginning before 2013

Acquired net operating losses are subject to limitation as determined under Internal Revenue Code section 382(g).

To complete the worksheet:

•Enter your Minnesota taxable net income or loss (Form M4NP, line 6) for the year in the Minnesota Taxable Net Income/Loss column.

•If the amount is a loss, add it to the total in the previous year’s Losses Remaining column and enter the sum in the Losses Remaining column. The amount of loss being used in each year is limited to 80% (0.80) of the taxable net income for the year.

If the amount is income, and you use the losses from previous years to reduce that income, enter the amount of loss used to reduce the income in the Minnesota Losses Used column.

Complete Schedule M4NP NOL and attach a copy with your Minnesota tax return.

You must complete a separate Schedule M4NP NOL for each corporation in a unitary group claiming a net operating loss deduction. Note: Organizations that file federal Form

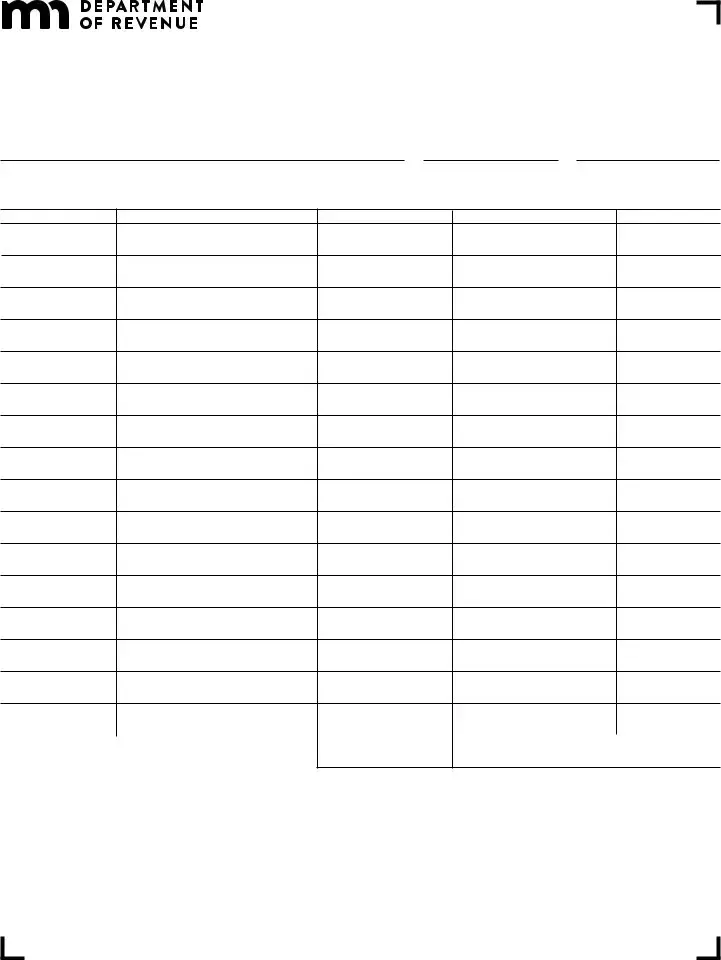

Example:

Year |

Taxable Net Income/Loss |

Minnesota Losses Used |

Minnesota Losses Carried Back |

Losses Remaining |

||

Oldest Loss Year |

|

|

|

|

|

|

12/31/13 |

(7,000) |

|

|

(7,000) |

|

|

|

|

|

|

|

|

|

Subsequent Year 1 |

|

|

|

|

|

|

12/31/14 |

4,000 |

(4,000) |

|

|

(3,000) |

|

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

12/31/15 |

(5,000) |

|

|

|

(8,000) |

|

|

|

|

|

|

|

|

3 |

16 ,000 |

(8,000) |

(8,000) |

|

0 |

|

12/31/16 |

|

|

||||

4 |

|

|

|

|

|

|

12/31/17 |

(13,000) |

|

|

(5,000) |

|

|

|

|

|

|

|

|

|

5 |

14 ,000 |

(5,000) |

|

|

0 |

|

12/31/18 |

|

|

|

|||

6 |

|

|

|

|

|

|

12/31/19 |

(7,000) |

|

|

|

(7,000) |

|

|

|

|

|

|

|

|

7 |

|

|

|

|

|

|

12/31/20 |

7,500 |

(6,000) |

|

|

(1,000) |

|

|

|

|

|

|

|

|

8 |

|

|

|

|

|

|

12/31/21 |

(1,000) |

|

|

(2,000) |

|

|

|

|

|

|

|

|

|

9 |

|

|

|

|

|

|

12/31/22 |

1,000 |

(800) |

|

|

(1,200) |

|

|

|

|

|

|

|

|

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

13 |

|

|

|

|

|

|

|

|

|

|

|

|

|

14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2022 Summary: |

Net Operating Loss Deduction |

Total Losses Remaining (to be carried forward) |

||

|

|

800 |

|

(1,200) |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

Enter on Form M4NP, line 7

| Fact | Detail |

|---|---|

| Purpose | For tax-exempt organizations and cooperatives that file federal Form 990-T or 1120-C to report Net Operating Loss Deduction. |

| Governing Law | Based on Internal Revenue Code section 382(g) for the limitations on acquired net operating losses. |

| Eligible Organizations | Organizations that file federal Form 990-T or 1120-C, excluding those that file Form 1120-H or 1120-POL. |

| Carry Forward Period | Net operating losses may be carried forward for 15 years. |

| Limitations | Net Operating Loss Deduction is limited to 80% of the organization's taxable net income for the year. |

| Carry Back Elimination | Starting with tax years after December 31, 2017, the two-year carry back option has been eliminated. |

| Apportionment | If income is apportioned to Minnesota, the unused net operating loss deduction is available at the apportionment percentage of the loss year. |

| Special Conditions | You cannot create or increase the net operating loss deduction with the deduction for dividends received or the foreign royalties subtraction for tax years beginning before 2013. |

| Attachment Requirement | Complete Schedule M4NP NOL and attach it with your Minnesota tax return. A separate form is required for each corporation in a unitary group claiming the deduction. |

| Completion Instructions | Enter Minnesota taxable net income or loss on Form M4NP, line 6, and follow instructions for calculating losses used and remaining. |

The process of filling out the Minnesota M4NP form is essential for tax-exempt organizations and cooperatives that need to report and apply their net operating losses against their Minnesota taxable income. This form plays a pivotal role in managing how prior year losses can offset current year taxable income, subject to certain limitations. Careful completion of the M4NP form ensures that your organization complies with Minnesota tax laws while maximizing potential benefits from past operating losses. Here is a step-by-step guide to assist in accurately completing the form.

Note: It is crucial to ensure that all applicable sections of the form are completed accurately to reflect your organization’s financial and operating status for the relevant tax year. Following the outlined steps will help guide you through the process of documenting and applying net operating losses and support an efficient and compliant tax reporting practice.

FAQs about the Minnesota M4Np Form

The Minnesota M4NP form is designed for tax-exempt organizations and cooperatives that file federal Forms 990-T or 1120-C. It is used to report and apply net operating losses (NOL) to offset taxable income. Specifically, it details the sources of net operating losses, the application of these losses against taxable net income in the current year, and the calculation of losses carried forward to future years. This is essential for organizations looking to maximize their tax benefits by deducting previous years' losses from their current taxable income.

According to the instructions for the 2021 Schedule M4NP NOL, the net operating loss deduction is limited to 80% of an organization's taxable net income for the year. Net operating losses can only be carried forward, not back, with a carryforward period of 15 years. This means if your organization incurs more losses than income in a given year, you can use those losses to reduce taxable income in future years, but only up to 80% of the income for any given year. This limitation ensures that some tax liability remains, promoting fiscal responsibility while still providing relief for struggling organizations.

No, not all organizations can claim a net operating loss deduction on the M4NP form. Organizations that file federal Form 1120-H (for residential real estate associations) or 1120-POL (for political organizations) are excluded from claiming this deduction. The M4NP form is specifically tailored for tax-exempt organizations and cooperatives that report unrelated business income on federal Forms 990-T or 1120-C, ensuring that those eligible for tax benefits can access them.

Unused net operating losses that are not applied against taxable income in the current year can be carried forward to future tax years. The carryforward period is 15 years, starting from the year in which the loss was incurred. These carried forward losses can be used to reduce taxable net income in subsequent years, subject to the 80% limitation. For instance, if losses exceed income in one year, the remaining loss (after applying the 80% rule) can be used to lower taxable income in the next year, providing a way for organizations to manage their tax liabilities over time.

Filing the Minnesota M4NP form, which is crucial for tax-exempt organizations and cooperatives reporting their net operating losses, can be a complex process. Unfortunately, mistakes can happen, but being aware of common pitfalls can help ensure the process goes smoothly. Here are six mistakes frequently made when filling out the Minnesota M4NP form.

Understanding these common mistakes and taking care to avoid them can help organizations accurately complete the Minnesota M4NP form, ensuring compliance with state taxation requirements.

When dealing with the Minnesota M4NP form, specifically designed for tax-exempt organizations and cooperatives to report net operating losses, it's important to gather and complete additional documents to ensure compliance and accuracy in reporting. Let’s explore other frequently used forms and documents alongside the M4NP:

Understanding and gathering these documents is essential for tax-exempt organizations and cooperatives in Minnesota when preparing their taxes. Each plays a vital role in ensuring compliance with tax laws, accurately reporting income or losses, and maintaining tax-exempt status. Therefore, thorough preparation and attention to detail with these forms can significantly impact the tax filing process for organizations.

The Form 990-T, also known as the Exempt Organization Business Income Tax Return, shares similarities with the Minnesota M4NP form. Both forms are used by tax-exempt organizations to report and calculate taxes on income that is not related to their exempt purpose. The Form 990-T is required at the federal level to report unrelated business taxable income, just as the M4NP is utilized within Minnesota for similar purposes. Key to both forms is the necessity to understand and apply deductions appropriately, including the handling of net operating losses, although the specific rules and calculations might differ due to the distinct tax jurisdictions.

Similar to the Form M4NP, the Federal Form 1120-C, used by cooperatives to report their income, deductions, and credits to the IRS, encompasses the reporting of net operating losses. Cooperatives, like tax-exempt organizations, have unique tax considerations and benefits, including the treatment of net operating losses that can be carried forward to future tax years. Both forms recognize the importance of net operating losses as a way to manage and mitigate taxable income across different periods, providing a mechanism for organizations to smooth out the fluctuations in their taxable income over time.

The concept of net operating loss carryforwards, integral to the Minnesota M4NP form, is also a key feature in the Federal Form 1120, the U.S. Corporation Income Tax Return. Corporate entities use Form 1120 to calculate their federal income tax liability, with allowances made for losses incurred in previous years to be used to offset potential taxable income, akin to the M4NP's treatment of losses. This parallel underscores the broader principle within both federal and state tax systems of acknowledging the financial cycles businesses and organizations experience, offering a form of relief during leaner periods through the use of past losses.

Form 990, the Return of Organization Exempt From Income Tax, shares a contextual relationship with the M4NP form in that both are designed for organizations operating within the tax-exempt framework, including nonprofits and certain cooperatives. While Form 990 primarily focuses on the disclosure of financial and operational information rather than the detailed tax calculations found in the M4NP, it serves as the backdrop against which tax-exempt entities must navigate their fiscal responsibilities. Both forms require detailed financial accounting and an acknowledgment of any income that could be subject to tax, emphasizing transparency and compliance within the non-profit sector.

When completing the Minnesota M4NP form, specifically aimed at tax-exempt organizations and cooperatives filing federal Forms 990-T or 1120-C, certain practices should be followed to ensure accuracy and compliance. Below are five recommendations on what to do and what to avoid.

Do:

Don't:

When it comes to the Minnesota M4Np form, there are several misconceptions that can lead to confusion for tax-exempt organizations and cooperatives. Let's address and clarify some of these misunderstandings:

Understanding these nuances about the Minnesota M4Np form can help organizations navigate their tax obligations more effectively and make the most of their financial planning strategies.

Understanding the intricacies of the Minnesota M4NP form can be crucial for tax-exempt organizations and cooperatives operating within the state. Here are five key takeaways to ensure proper completion and utilization of the form:

By carefully adhering to these guidelines, tax-exempt organizations and cooperatives can effectively navigate the complexities of the M4NP form, ensuring compliance with Minnesota tax laws while optimally leveraging net operating losses to reduce their taxable income.

Minnesota Ec04 - Employees can use this form to request a hearing with a compensation judge if there's a dispute with the insurer regarding the claim.

Minnesota Ig257 - Dedicated sections for the contact information of both the insurance company and a preparer, if applicable, ensuring clear communication channels.

Mn State Tax Form - If additional tax is due after initial filing, the IG260 form includes instructions on how to submit separate payments for each period.